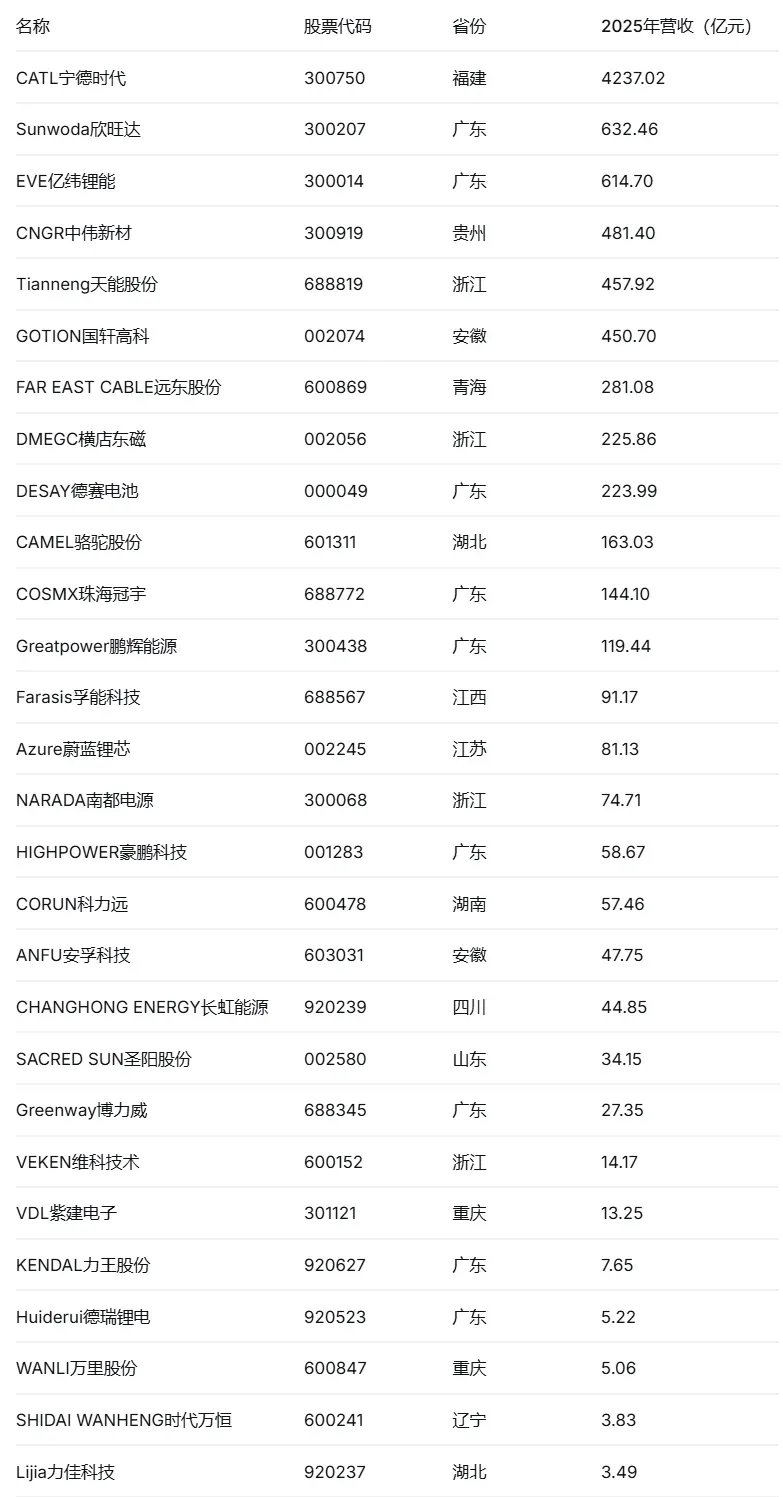

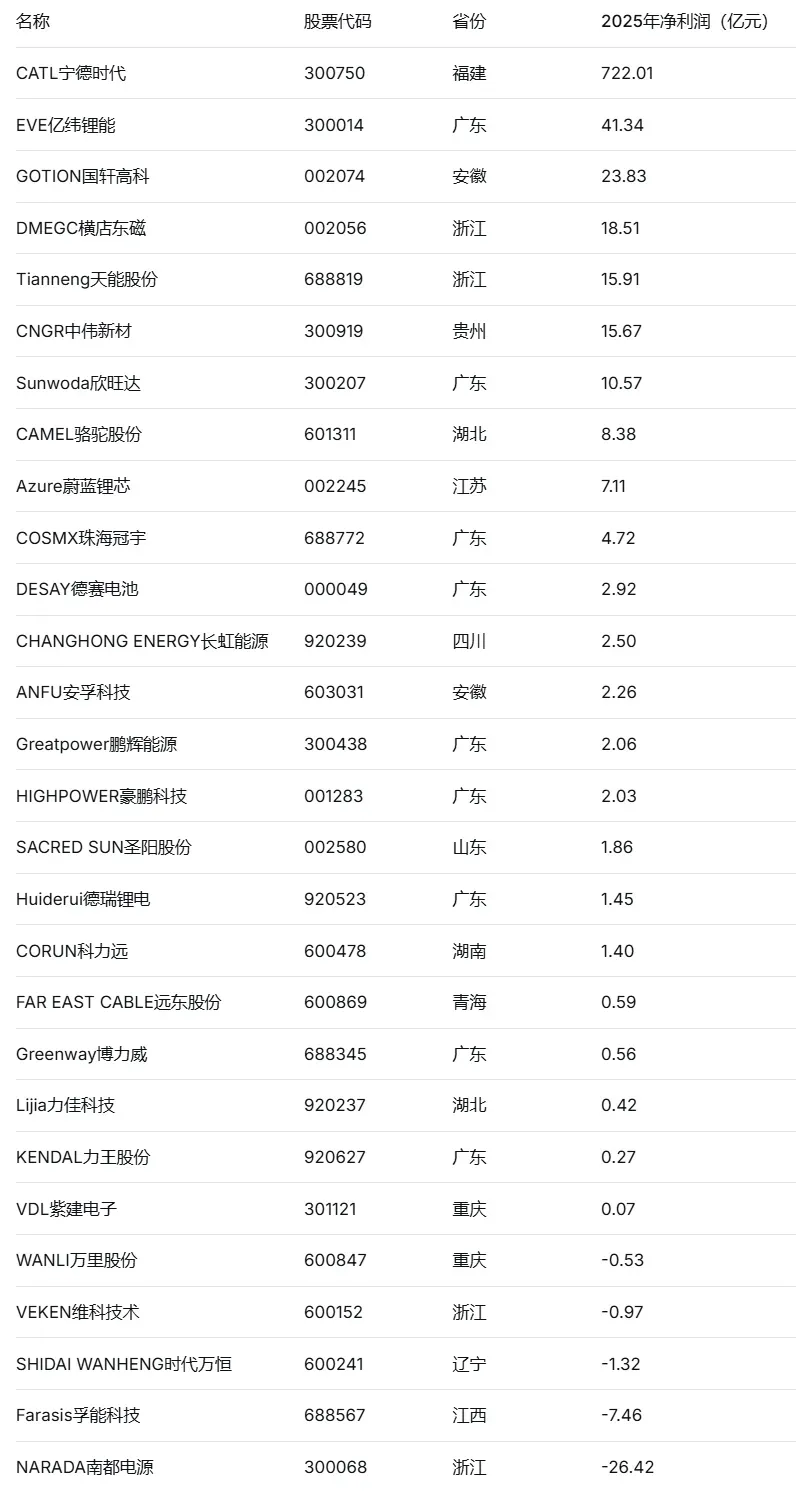

The 2025 financial data for 28 A-share battery firms tells a story of an industry moving towards extreme polarization. With companies heavily clustered in the Pearl River Delta and Yangtze River Delta, the top 20% of players are effectively controlling 80% of the market. With the top three firms generating over 83 billion RMB in combined profits, the gap between market leaders and the rest is widening. As the industry matures, the survivors will be those that master the art of global scaling while maintaining a lean cost structure.

The hierarchy is clear. CATL sits at the top with over 420 billion RMB in revenue, leaving the rest of the pack, led by Sunwoda at 63.2 billion RMB, far behind. The profit gap is even more telling: CATL’s 72.2 billion RMB net profit dwarfs the competition, with EVE Energy trailing in second at 4.1 billion RMB. While established giants thrive, some larger firms have stumbled, reporting losses of over 100 million RMB due to poor cost management. Interestingly, newer entrants on the Beijing Stock Exchange, such as Changhong Energy, have shown remarkable resilience and steady profitability.

The race is no longer just about revenue; it’s about profit margins and cash flow. While the heavyweights continue to dominate the global scene, mid-market players need to pivot. Whether it's carving out a niche in energy storage, building localized plants overseas, or betting on cutting-edge proprietary tech, the strategy must change. For the battery makers of tomorrow, success will depend on one thing: the ability to maintain a flexible, cost-efficient supply chain in a tightening regulatory environment.

Related Articles:

1. Full-Tab Battery Cells Inside! Sharge 300W Power Bank Launches on Kickstarter

2. 2026 EVE Energy Consumer Battery Product Catalog

3. One-Tap Battery Health Check:UGREEN P6 Series 45W Power Bank with Integrated Cable Now AvailableinChina